Tokenized Markets Lack Infrastructure, Not Assets

April 23, 2026

Tokenization Has a Market-making Problem

Trillions of dollars in real-world assets are being issued onchain, but the operators required to make those assets genuinely tradeable at institutional scale have not kept pace. Without dedicated liquidity providers bridging fragmented venues, the gap between what tokenized markets promise and what they can actually deliver will only widen as the market grows.

Earlier this month, the IMF effectively broke down this issue. In a paper by Tobias Adrian, Director of its Monetary and Capital Markets Department, the IMF described tokenization as a fundamental reconfiguration of global financial architecture while flagging four core systemic risks: fragmentation, stability amplification, cross-border resolution complexity, and emerging market instability. Each of these issues traces back to today’s onchain market-making gap.

What the market needs now is not more assets, but the infrastructure and operators that make them genuinely tradeable. Closing this gap is the defining challenge of the current market cycle.

Asset Tokenization Is Outpacing Market Making

To date, capital and engineering attention have flooded into the asset layer of tokenized finance, creating the rails, wrapping the treasuries, and establishing the legal frameworks that allow real-world assets to exist onchain. The tokenized U.S. Treasury market alone blew past $10 billion this January, and Standard Chartered projects the total tokenized RWA market will reach $2 trillion by 2028.

But once a tokenized asset is onchain, someone still needs to hold inventory, bridge pricing gaps, and provide two-sided liquidity across venues. Liquidity providers are the operators who do this work. When they operate well, every buyer and seller benefits through tighter spreads and more reliable prices. When they are absent, even a well-designed asset becomes difficult to use at institutional scale.

This is the work the tokenization industry has not adequately invested in. Even as capital floods into asset creation, the actual act of making those assets continuously tradeable and practically useful once they exist has become a growing need. As a result, despite the billions now sitting in tokenized RWAs, most of that activity reflects asset issuance and institutional allocation batching rather than active secondary trading.

Faster Rails Do Not Produce Deeper Markets

A common response to the liquidity gap is that it will resolve itself as settlement infrastructure matures. The idea is that atomic settlement, faster finality, and programmable execution will naturally close pricing dislocations as they emerge. This argument is based on the belief that if capital can move frictionlessly between venues, arbitrage should do the work that dedicated market makers would otherwise do. But while settlement speed is now lightning-quick across many onchain markets, faster rails address a different problem than the one major tokenized markets now face.

Consider what fragmented settlement infrastructure already costs in traditional markets. Global equity markets lost $96 billion in 2023 to settlement failures and the margin infrastructure required to prevent them. According to Euroclear, 71% of those failures stemmed from counterparty shorts. a consequence of fragmented infrastructure and thin liquidity, not slow rails.

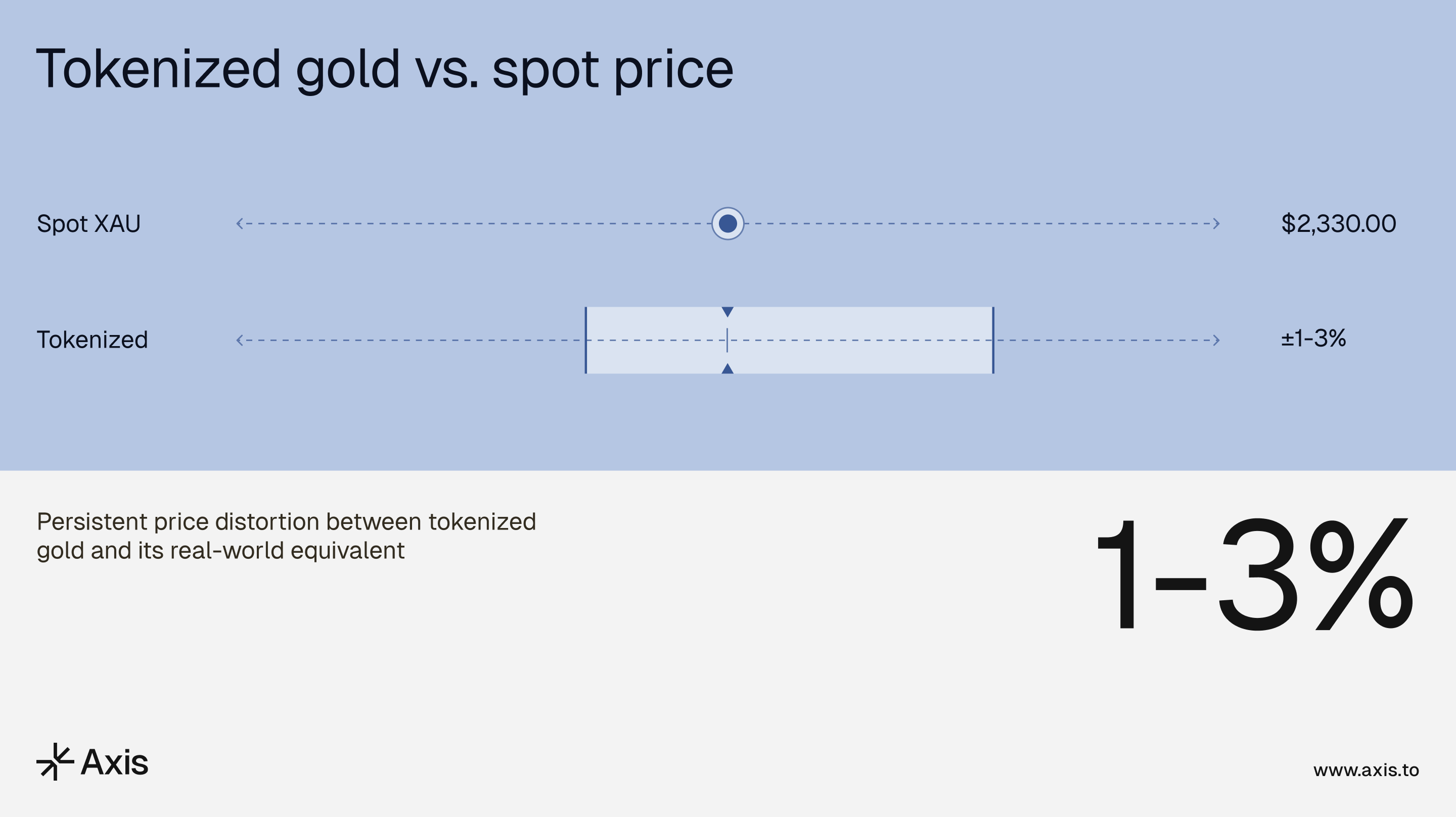

Onchain markets are based on entirely different financial rails, but they suffer from a similar underlying dynamic. Tokenized assets like gold regularly trade at 1-3% price distortions relative to their real-world equivalents. That is most likely a liquidity provision problem and a direct consequence of the active market-making layer not yet existing at meaningful depth.

What makes this more counterintuitive still is that improving settlement speed actually intensifies rather than relieves this pressure. As the IMF’s paper notes, as "settlement becomes continuous, margining becomes automated, and liquidity demands materialize instantaneously." In a T+2 system, a market maker can net positions across a settlement cycle and reduce the inventory required to maintain continuous quotes. But in a real-time environment, every position must be funded immediately, across every active venue, simultaneously.

Every Mature Market Needs a Deep Liquidity Layer

The history of every major asset class makes the solution clear. Equities, FX, rates, and commodities markets all required a dedicated professional liquidity layer before broad institutional capital allocation followed. The firms that built that infrastructure did so by systematically closing the dislocations that fragmented venues produce, making those markets more accessible and more useful for every participant within them. Without that dedicated market making layer, liquidity fragmentation simply compounds over time.

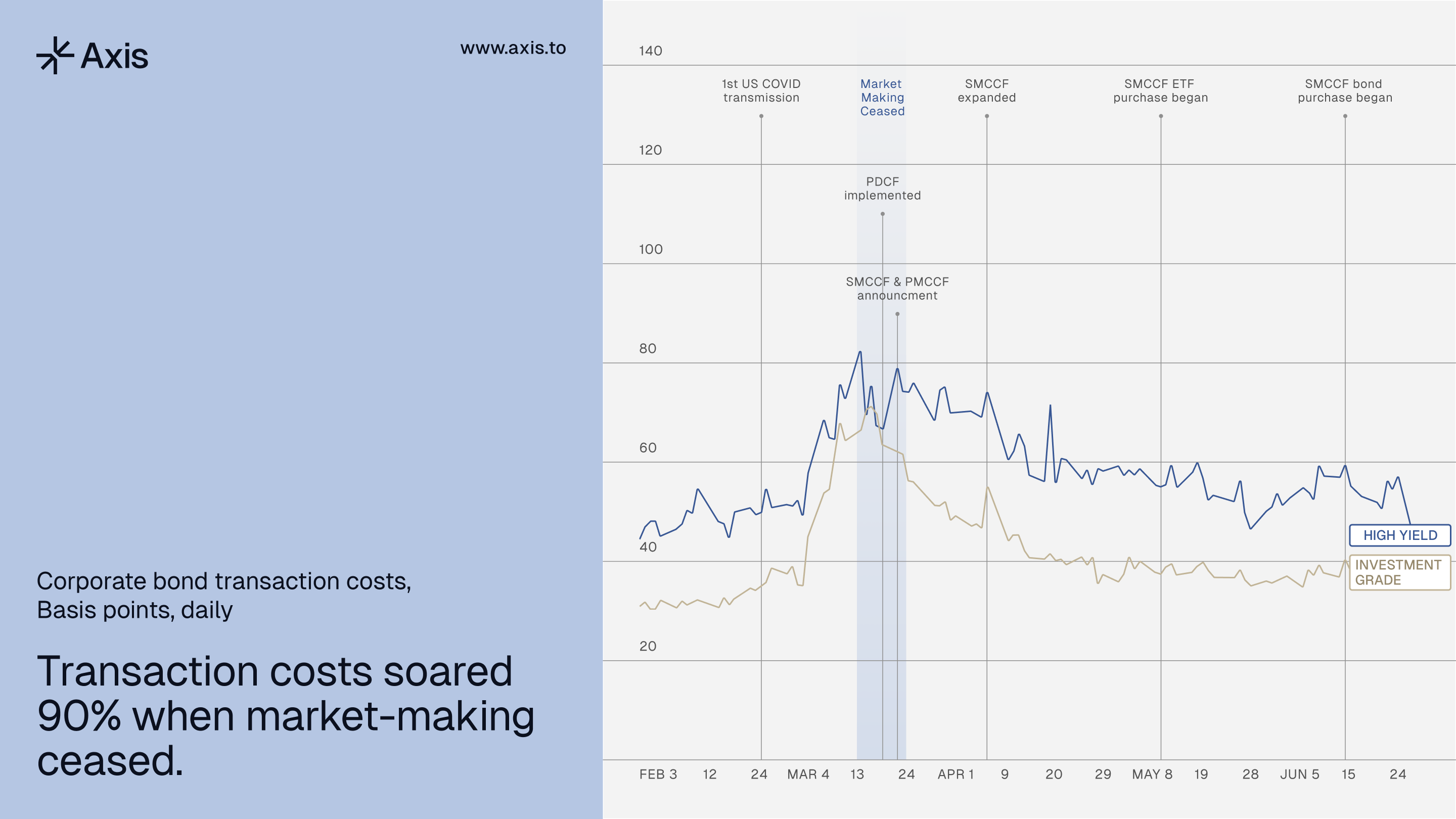

The corporate bond market offers the clearest illustration of what happens when that layer fails. In March 2020, as selling pressure surged, dealer balance sheets hit their limits and market-making effectively ceased. Transaction costs soared 90%, bid-ask spreads widened to 150 basis points, and bond mutual funds saw net outflows exceeding $250 billion in a single month. The problem was not the quality of the underlying assets. It was the absence of operators with sufficient balance sheet capacity to absorb flow when conditions deteriorated. The market only stabilized after the Federal Reserve stepped in directly with emergency liquidity facilities.

Tokenized asset markets are in the process of building their own version of this infrastructure from scratch, across a far more fragmented landscape. The conditions that caused the 2020 dislocation will recur in tokenized markets, but potentially even more quickly and severely since automated execution and continuous settlement leave less time for intervention.

The Race to Define Market Structure

What tokenized finance needs is not just better technology or clearer regulation. It needs operators whose entire model is built around fixing the fragmentation itself, holding balance sheets large enough to route capital between markets and asset classes that would otherwise remain disconnected.

The IMF's paper concludes with a declaration that "the window for shaping the architecture of the tokenized financial system is open, but it will not remain so indefinitely." In short, new markets are malleable, but only for so long. The firms that built institutional liquidity infrastructure in equities and FX did so early enough to be rewarded and before the market consolidated around dominant players.

The firms building this capability now are constructing the foundational infrastructure that determines how quickly tokenized assets reach a multi-trillion dollar market cap, and how broadly that value can spread.

Axis Helps Close the Liquidity Gap

Tokenized finance is in the same market-making inflection point legacy markets overcame in the past, and Axis is built to help close the gap—not as a single-strategy trading operation, but as a cross-venue, cross-asset, cross-jurisdiction capital layer that connects markets to the rest of the onchain ecosystem depends on. With 36% annualized returns, a 4.9 Sharpe ratio, and $400 million in historical peak AUM, the approach reflects a repeatable process for identifying and closing the pricing gaps that fragmented markets produce.

The institutions and individual users that tokenized finance is being built to serve all depend on capital that can move between fragmented markets reliably, at speed, and at fair prices, and that is precisely what Axis makes possible.

In the coming weeks, Axis is launching its public Transparency Dashboard, allowing the market to watch our institutional arbitrage engine generate performance in real-time. Follow us on X for early access, and for ongoing analysis of the market structure dynamics that move prices before they show up in the headlines.